Annual message that forecasts are useless

2026 Edition

It’s December and this lovely time of year filled with celebrations and family gatherings is unfortunately also overrun by rearview mirror performance reviews and the some how required outlooks for the year ahead. My suggestion is to not read any of them. My even stronger suggestion is that if your portfolio is set up properly today under no circumstances should you feel the need to adjust it for 2026. No one knows what will happen over the course of next year.

Those writing outlooks have various incentives to write. Some must write because they work for an institution that requires them to write. Others write because they want to put a stake in the ground to be able to prove to their paying clients that they made a good call a year later. Some purely altruistic writers publish outlooks for no financial or ego gratification incentive and simply offer their thoughts to the world for free. Whether the incentives are pure and aligned with your personal investment success or perhaps are partially aligned with you paying them commissions or fees makes no difference. No one knows what will happen over the course of next year.

Tl;dr Your job is to have a portfolio of assets that has a risk that you can tolerate and is balanced and diversified to provide the highest odds of success whatever happens in 2026 and ignore all advice to shift your balance to something else and go about your life.

The great thing about this approach is a balanced and diversified portfolio grows your wealth and maintains your purchasing power with very little “management”. The occasional rebalance and perhaps some tax management is all that is necessary in 2026. You and almost all (probably all that you could ever have access to) cannot time markets. DON’T TRY. If you MUST read someones work on investing start with how to build this balanced diversified portfolio here. Better would be to enjoy the holidays. Stop reading this!

Okay you want my forecast anyway?

Im not giving it to you because its useless and I will be either randomly correct or most likely wrong. Stop reading.

Maybe this would be valuable for your holiday reading - probably not tho.

As you are still here, what I will attempt to do in the rest of this article is provide a completely objective description of the drivers of equity returns over a one year horizon for you to weight in whatever way you would prefer. This will hopefully be a roadmap for how you can better navigate the actual events and market reactions that play out over the next year. I’d rather provide a roadmap than a destination.

Anchoring vs humility.

Why put a target down? Immediately on writing down a target, or reading and believing in that target, the target becomes an anchor. The target biases ones ability to adjust to an ever changing market and economic landscape. Which brings me to humility.

Our lives are defined by our daily choices and actions. We make choices based on information we have and our hope that we chose the best action that will work for our future selves. We can’t predict the future. We do the best with the information we have and accept the outcome. However our daily choices may have well defined consequences that manifest immediately or over time with high certainty. For instance if we choose to grab a hot pan from the stove without a potholder we are choosing the chance of getting burnt vs the time saving nature of not locating the potholder. A burn is a known consequence and we are just weighing the odds. We have lots of experience with this choice. We may be fairly expert at determining the chance of the burn due to that experience. However this choice including most of our daily choices that we are well prepared to make has risk.

On the other hand when looking at making a choice to buy or sell an asset our success depends on being able to evaluate the future and MUCH more importantly being able to beat the rest of the people trying to evaluate the future. I have said often, over the years and throughout my career, that I probably have no ability to beat the markets. Why? I have worked at a few of the greatest trading and investing firms in history. I have met and gotten to know many of the greatest investors ever born. I have systemized trading strategies that allow computers to more quickly and less emotionally implement the strategies of these great investors to beat them at their own game. What I know with certainty is that I do not have what it takes to beat these guys. I have spent at least 120,000 hours over my almost 40 year career thinking about, researching, and trading markets, I have access to data and analytical tools that you do not. However, my old firm Bridgewater Associates has 100 people working 12 hour days every day trying to beat me. Now they even have AI trying to beat me. Their data sourcing budget is at least 100X mine. Even if they started today they would be ahead of me in less than 3 months. They’ve been at it for decades. Thats just one firm, dozens if not hundreds of firms are as dedicated to beating me but they don’t care about beating me they are trying to beat each other and simply survive. Thousands of firms have more resources and place more effort in beating markets than I do. Every morning of every day I start with the humbling fact that I stand little or no chance in beating markets. Perhaps you can STOP READING and Scroll up to the top and reread what a humble person does.

Okay I’m humble why is anchoring a problem?

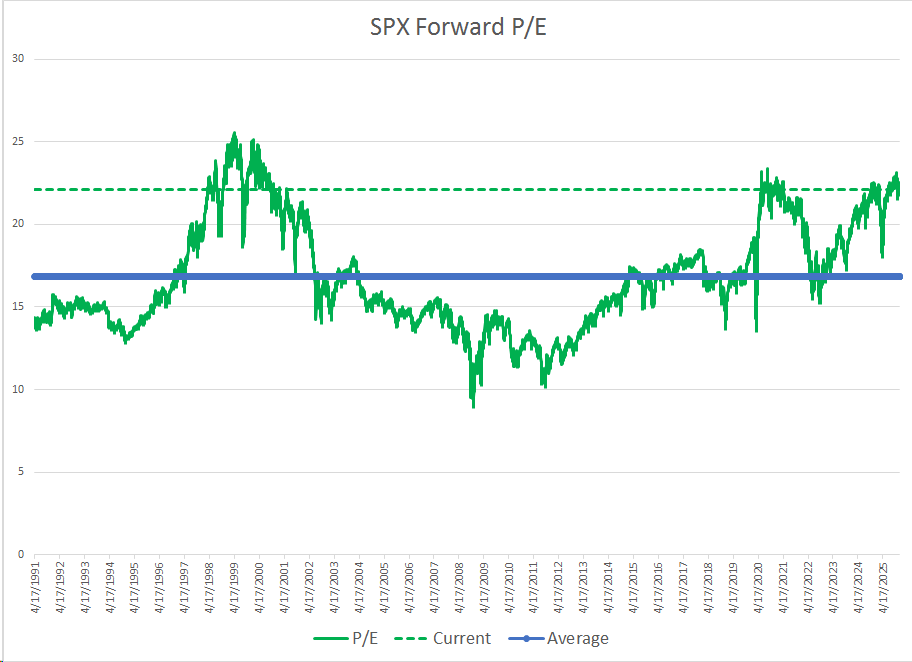

Anchoring is saying the market price is wrong. Humility says the market price is always correct. Every day those who try to beat markets look for answers. One of my favorites is versions of this one. I even print this in my work. Its a classic anchor.

One can look at that chart and conclude “Equities are almost as rich as they were in the tech bubble and look at what happened then!” BUT implicit in that statement is that markets are mis-priced today. It shows a lack of acceptance that everyone involved with markets already has this information. I want to be clear. I am not saying that a high P/E won’t revert to a long run average one day. I think it probably will. I am simply saying that an anchor such as this if weighed heavily in ones choices is death to most investors as it is hubris instead of humility.

There are two options in my mind. Accept that you don’t know shit about markets relative to those you are trying to beat and don’t try, or only very loosely anchor your views and remain openminded about things that could change your view.

My point is that a target creates a meaningful anchor. Balance any anchor in your process lightly vs humility.

If you have read this far I’ll now actually say what I think matters to equities over the course of the year 2026 and any other year in the future.

My friend Bob Elliot captured the primary reason for equity returns in this tweet.

Corporations who issue stock use the proceeds to generate long term value for shareholders by creating productivity. They also pay shareholders a risk premium each day as compensation for the cash they invest. So once again holding stocks as part of a balanced portfolio over the long term rewards investors by paying a risk premium and generating real productive growth. Okay thats fine. Now what about the wiggles in 2026.

My framework looks at major drivers of assets including stocks with 3 pillars.

Actual growth relative to expectations and changes in growth expectations

Actual inflation relative to expectations and changes in inflation expectations

Risk premium changes which are impacted by

changes in expected risk of the asset and portfolios in general

demand for assets from savers for investment and supply of assets from issuers

cost and availability of credit for investors to make leveraged asset purchases

So let’s assume for the moment that no anchors exist, nothing reverts to a mean, momentum is a short term front running of a shift in the above drivers and essentially the current market price is perfectly fair. By doing this we accept that the SPX close of 6834 is fair and perhaps a change in any of these drivers could cause a change in price of 5% up or down relatively symmetrically in the next few months.

Let’s look at growth

More growth in the economy relative to expectations is a bullish pressure stocks. Real growth depends on a number of things. Its trend is determined by population growth and productivity growth. Its wiggles depend on leveraging up and down.

Population growth expectations are part of growth expectations. Going into 2026 population growth has fallen markedly as our borders have been closed. However, expectations have now adjusted to that fact. Changing the amount of citizens in the work force is extremely slow moving. Changing the amount of workers in the work force in 2026 will depend (like most years) on immigration policy. The Trump administration seems committed to policies implemented in 2025 which have caused a flat line in population growth. Expectations reflect continued slow or no immigration. Making no judgement on the topic of immigration and simply linking its impact to real growth the bull case for stocks is for a rise in immigration relative to the recently lowered actual immigration and future expectations. Slower population growth causes slower real growth and slower population growth is already consensus expectation.

Productivity growth expectations are also part of growth expectations. Since Covid the U.S. has been the envy of the world as its productivity has massively outperformed the rest of the world and is running near historic high levels. Theories abound about why. I favor the idea that our workforce was meaningfully disrupted with 20% unemployment and rapid reemployment which resulted in a more efficient allocation of our labor force in jobs that better matched skills. In addition, the change in work from more gig economy and work from home likely had an impact on our aggregate productive output. Lastly a large increase in immigration also likely took advantage of workers with low productivity being aided by American productivity enhancements and on the job training to get lots more output from a new worker.

Looking forward the 2026 expectations for productivity growth is most certainly higher than it was before the election. The administration promises massive deregulation which would increase productivity. Deregulation may or may not be long term good for society around consumer protection, worker protections, and financial stability (I remember a bunch of financial system deregulation going quite badly) but thats for the longer term future to see. Deregulation is productivity enhancing and is coming. So once again it comes down to expectations. Will deregulation happen more or less than expectations and will it add more or less to productivity relative to expectations. The bull case for equities depends on productivity improvement greater than recently elevated expectations.

The other major development regarding productivity is AI. Consensus is that AI will one day increase productivity, as we mentioned in last year’s useless forecast note 2025 was gong to be early. It seems to us that a year later no real progress has been made such that AI will have a major positive impact on productivity but expectations remain rosy. Bringing AI driven productivity increases forward in time and/or larger in impact relative to current rosy expectations would be bullish equities.

The last big impact on real growth is growth financed by debt. The sources of debt financed growth are banks and fiscal deficits. Bank debt growth since Covid has been slower than GDP and remains slower than GDP but is rising recently. Government debt financed growth peaked during Covid and the year that followed. The scale of that debt growth was enormous. Looking forward bank debt growth could meaningfully increase growth expectations if it were to accelerate and would be bullish stocks. Keeping track of bank debt growth is critical to understand future growth.

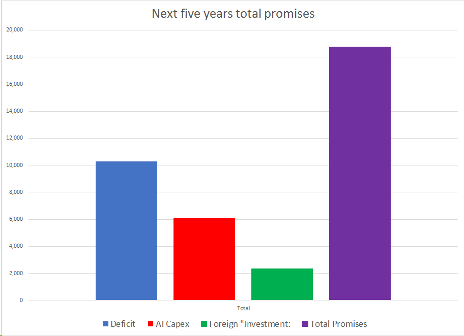

Perhaps the biggest factor we see for 2026 and beyond is the promises of capital investment made by, the private sector to fund AI capex, both the private sector and foreign governments to invest in US based production capacity for onshoring, and of course the ongoing deficit which continues to run at 6% of GDP.

Over the next 5 years promises of close to 20TN of US investment above the already large funding requirements of the US economy have been made. This is massive debt growth. These plans for massive debt growth are built into growth expectations already. Changes in the amounts of debt relative to expectations would impact equtiy markets. I have written a Damped Spring Report for clients of dampedspring.com which outlines the promises made and more importantly the ability for capital markets to absorb the supply of debt here.

The 2026 outlook for the Government debt financed growth looks highly uncertain. The administration has reduced the deficit by increasing tariff revenues and modestly cutting spending on the weakest cohort in the economy while offsetting that negative growth hit with broad tax cuts. Overall the 2025 deficit is lower than 2024 primarily driven by short term spending cuts and tariff revenues. Tariff revenues remain at risk as the SCOTUS is working on their ruling on whether tariffs are illegal. If they rule that tariffs, as implemented, are illegal the administration has promised to institute tariffs of similar size through legal means. Markets expect that the tariffs will be declared illegal and the new legal tariffs will be smaller but still sizable. The OBBB impact for 2026 due to tax cuts is expected to increase the deficit realitive to 2025 which is modestly stimulative to growth. Further bullish actions by the administration such as another reconciliation effort in the spring is highly likely and thus expected to focus on tax rebates and tax cuts which would grow the deficit. I do not expect that significant spending cuts will be part of that reconciliation but its hard to know how the administration will be able to garner enough votes for a deficit increasing reconciliation so spending cuts are still on the table. One clear outcome is if the administration convinces the reticent republican senators to use the nuclear option and bust the filibuster in order to push through their agenda the odds of a stimulative pre mid terms impulse would jump. If that path is chosen we would expect some growth in the deficit while also expecting some significant spending cuts. Regardless, changes in the deficit are small relative to the big promises made mentioned above.

Inflation - Sticky and nuanced impact on equities

The linkage to equity performance and inflation is much weaker than the impact of real growth. Inflation itself is caused by different drivers our own framework for inflation has three pillars. Each pillar was in force since covid and each one has different impact on equity prices.

We believe inflation occurs based on three factors

Supply constraints. Supply can become restricted for various reasons, Oil Embargoes in the 70’s and the supply chain disruptions of Covid standout but of course natural disasters, factory and worker capacity and many other factors can affect supply

Demand can increase faster than supply. This could be, a culture shift from thrifty to spendthrift, an expectation of inflation can accelerate inflation itself, and workers can demand more compensation as a share of corporate profits when labor has leverage. Lots of theories exist on demand driven inflation in this particular cycle demand has been very strong driven by wages and wealth.

Monetary inflation. Simply put if every physical and digital USD was cut and half and each half “spent” like a full old dollar prices of assets and most everything would double. While many believe this is the only source of inflation (and they may be correct based on the assumption that 1 and 2 above are transitory) we treat it separately as transitory demand and supply inflation can last long enough to impact policy makers.

The flow through of inflation to equity returns depends on what is inflating and why.

Inflation of final goods and services increases top line revenue. Because companies have a set of relatively fixed expenses and increase in both top line revenue and variable expenses results in margin expansion and is bullish equities. However to the extent that top line inflation is lower than expense inflation margins can contract. Monetary inflation is good for equities in nominal terms. But its important to state that inflation has an impact on monetary policy. When it is above target policymakers use their tools to lean against inflation. If those tools are effective (which is unclear to us this cycle) then rising inflation can be bearish equities as the policy tightening increase the value of cash relative to assets.

Over the last five years, even at peak inflation, expectations for inflation measured by where market expected inflation to realize five years forward never de-anchored

The markets expected the impact of Covid’s supply chain disruption, the 6TN of stimulus paid to support consumption, and the huge burst of pent up demand that occurred when the economy reopended to be transitory. Given the relatively sizable actual realized inflation and the significant selloff and recovery in assets prices one would think that inflation mattered a lot to equity returns. This is not clear to me. However if inflation expectations fall to target I expect that would be bullish equities driven primarily by the Fed being able to remove any sort of monetary restrictiveness. However as we enter 2026 the market is already priced for the removal of monetary restrictiveness and further easing would be required to be bullish equities. I expect a dovish Fed Chairman and so on net think easing is coming and marginally bullish for equities.

Looking forward as mentioned inflation expectations are largely anchored and are currently near target. Measured inflation is high and well above target but well below peak.

The Trump Tariffs have increase price levels and have been inflationary. They are in the rearview mirror by and large. While the SCOTUS decision, the subsequent remedy if needed and reinstitution of legal tariffs creates some wiggles we do not expect significant increases in tariffs

As mentioned above immigration expectations impact growth and not surprisingly impact inflation. Our simplistic framework is that people of all sorts produce more than they consume. Thus one less worker will be anti growth and pro inflation. The economy will get one less unit of production and less than one unit of less consumption. Net less supply and thus less growth and more inflation. Once again less immigration restriction than expected would be disinflationary and allow the policymakers to ease. I think the inflation linkage to equity performance is soft but as I see no change in immigration but an easing on immigration restriction if it occured would be bullish equities as I think disinflation would drive easier policy.

Deficit reduction is both anti growth and disinflationary by reducing demand and reducing fiscal impact on monetary inflation. If deficit reduction is less than expected the increase in inflation pressure offsets some of the bullish growth impact but is likely not as strong.

Deregulation is disinflationary and positive for equities. Deregulation expectations would have to rise vs current levels to be bullish equities

The AI Boom is long term disinflationary when the productivity impulse is realized. It is also short term inflationary as the investment in capacity pushes up wages and prices. Expectations remain rosy for the productivity impulse and relatively muted for the inflationary impact of the investment spending boom. Not a great set up for inflation tbh.

In summary, Inflation expectations are already quite low. Adding up both the expectations of policy impacts and the current realized warm inflation its possible to create a bull case for equities but seems marginal. Similarly a bear case for equities based on inflation alone would really need to be caused by both actual inflation coming in hot and inflation expectations rising. Its possible either case could be impacted by Fed policy as well over the year.

Risk premiums

The most powerful reason to own equities over the long term is that they reliably offer and excess risk adjusted return over cash. In this thread I explain risk premiums

In order to harvest risk premiums on equities or risk premiums from a portfolio of assets that each provide risk premiums one must buy and hold for a long time. The reason is that the level of risk premium offered can vary meaningfully in the short term, in addition risk premium can be delivering its daily small dose of outperformance and a change in growth or inflation can result in a drawdown that would swamp risk premium collection. So I prefer holding assets that diversify away growth and inflation related drawdowns and just collect risk premium.

But this is about what drives equites over the next year and what factors are likely to impact equity risk premiums during that time. Thankfully risk premiums linkage is straight forward. When risk premiums fall equites rise.

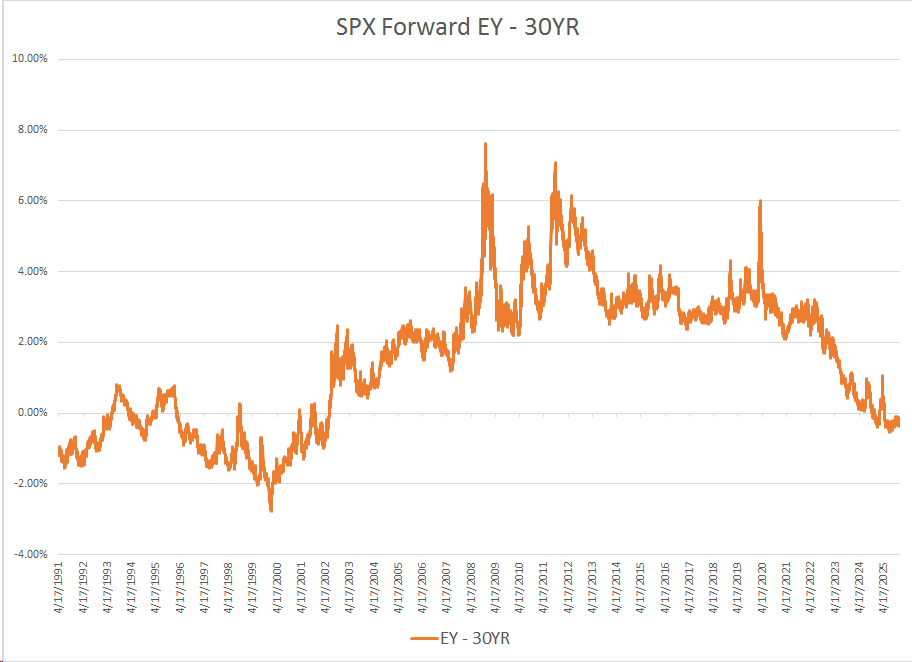

First a warning. There are rough heuristics for risk premium. P/E multiple is one. Rising P/E = falling risk premium. Another is Earnings Yield - Risk Free Rate. That seems slightly more mathy. Most people who are selling you an anchor will show you this chart and include the time back to 1996 as “proof” that this heuristic shows a very low “Risk Premium” except when the stock market was in a buble. But looking farther back 1990-2000 was a full decade where stocks were “Expensive”. Remember humility?

Risk premiums can only be modeled as they are unobservable. The more “accurate” the model the more likely that it is dominated by future growth expectations for earnings. So why bother discussing?

You can’t see risk premiums but knowing what drive them can help

Risk premiums change due to three basic factors

changes in expected risk of the asset and portfolios in general

demand for assets from savers for investment and supply of assets from issuers

cost and availability of credit for investors to make leveraged asset purchases

If for some reason you expected holding stocks to be less risky but still have the same expected return going forward than they have had, all else equal you would want to hold more of them. Falling expectations of risk for equities is bullish. When considering whether one is bullish or bearish equities one is making an implicit bet on future risk.

One of the most discussed topics in investing and in fact the topic my last substack article is the outlook for demand of stocks from “passive investors” Here is a link to that article. For purposes of this article the demand from savers is driven by GDP which delivers income to the economy and on to savers for investment in assets. Risk premiums contract when demand from savers is inelastic and supply is quite elastic. But as all things we know that markets are fairly priced and thus see the passive demand coming based on some expectations of the driver of passive demand. Thats mostly nominal incomes. The bull case for equities driven by demand flows of passive investors is for nominal income growth to exceed expectations. More savings lower risk premium higher prices. Easy. The 2025 policy sensitivity to savings can be seen above in those things that drive nominal savings, however the weeds of the budget deficit policy and its expectations are meaningful. Tax policy that reduces the tax burden on household savings is bullish stocks. Tax policy that reduces the burden on corporations is bullish stocks due to earnings but isnt bullish particularly due to risk premium contractions as the tax savings will not likely be invested in equities. Expenditure cuts reduce the savings of the private sector. That is bearish equities apart from the hit to growth. Simply put in order to offset expenditure income and continue to spend the private sector needs to dissave and sell equities. Which brings us to expectations. If tax policy takes less of a bite from households than expected thats bullish equities. If expenditure cuts are less than expected thats bullish equities.

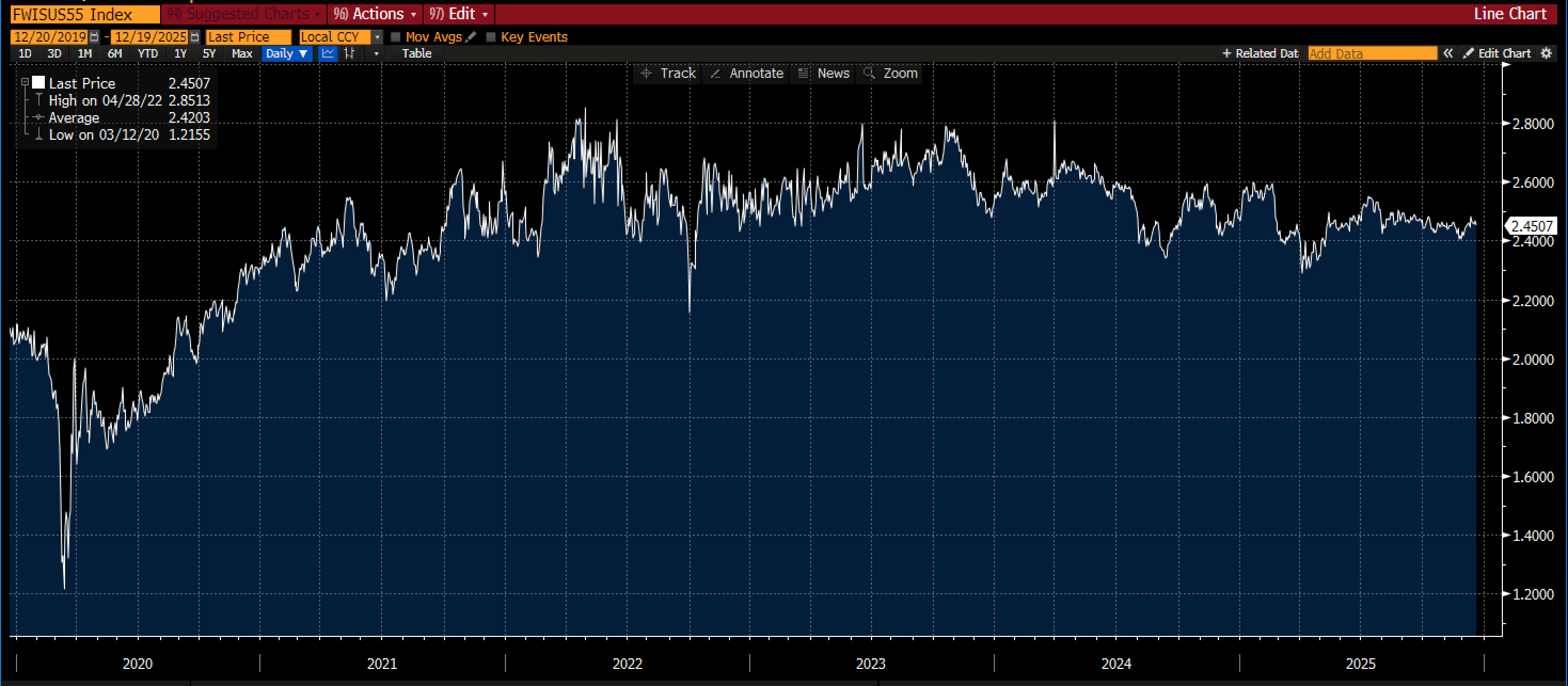

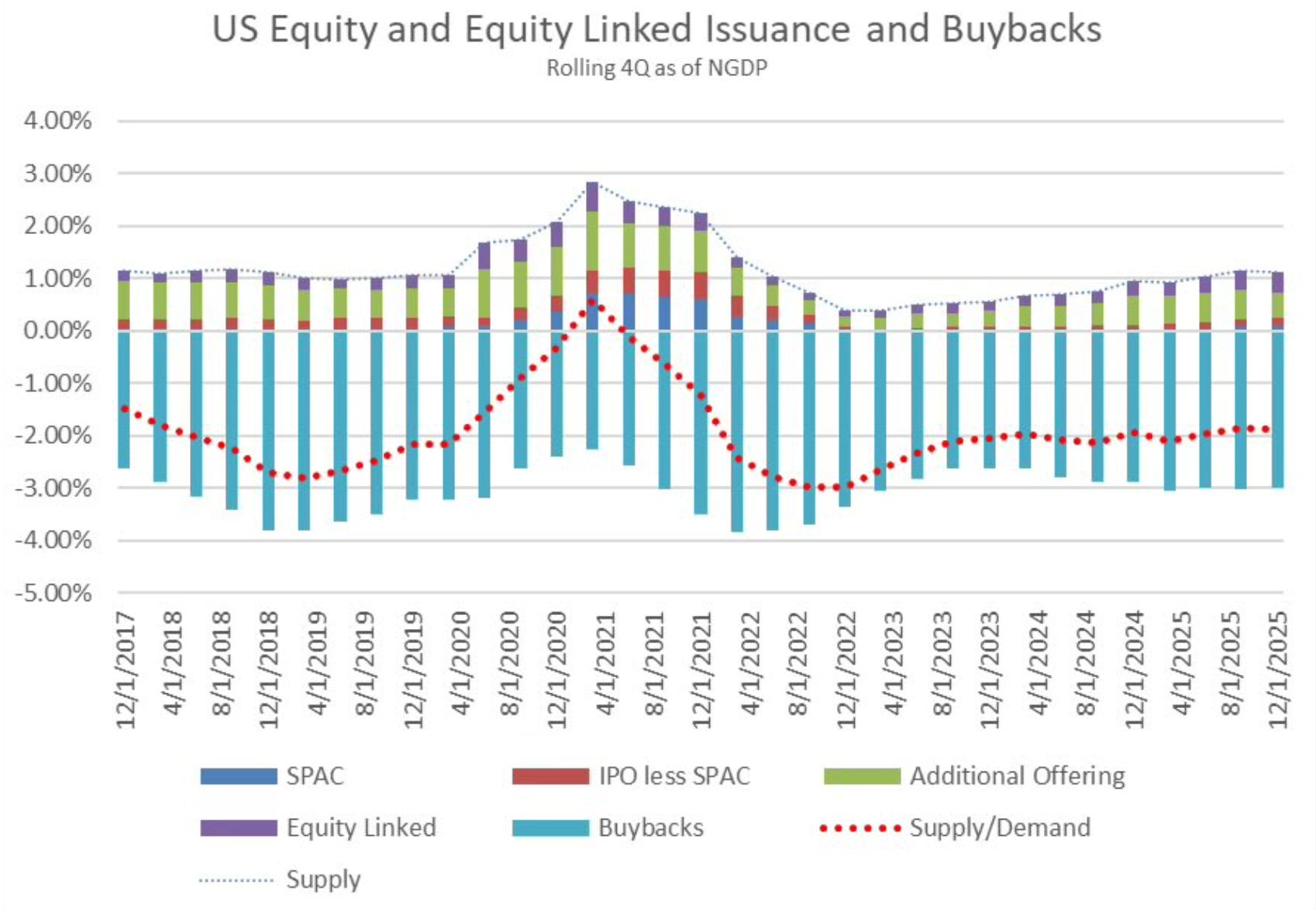

I addressed savers they represent demand for stocks. What about issuers who are the supply of stocks? New equities for savers to buy comes from a few places. IPO’s result in new public companies, secondary offerings sell equity on behalf of the company to fund its growth or its original private investors, insiders of the company recieive and sell shares in lieu of cash compensation and that creates more stock to meet demand. Even convertible bonds can issue equity like assets to the savers. Supply of this sort is always present in markets but is also variable depending on pricing and need of corporations for financing. Let’s get to the elephant in the room. Companies are NOT issuing new shares. In fact the opposite. Companies and particularly the Big cap stocks are actively reducing supply in the private sector via share buybacks. In fact supply of shares has been declining at a rate of 2-3% of GDP over the last few years.

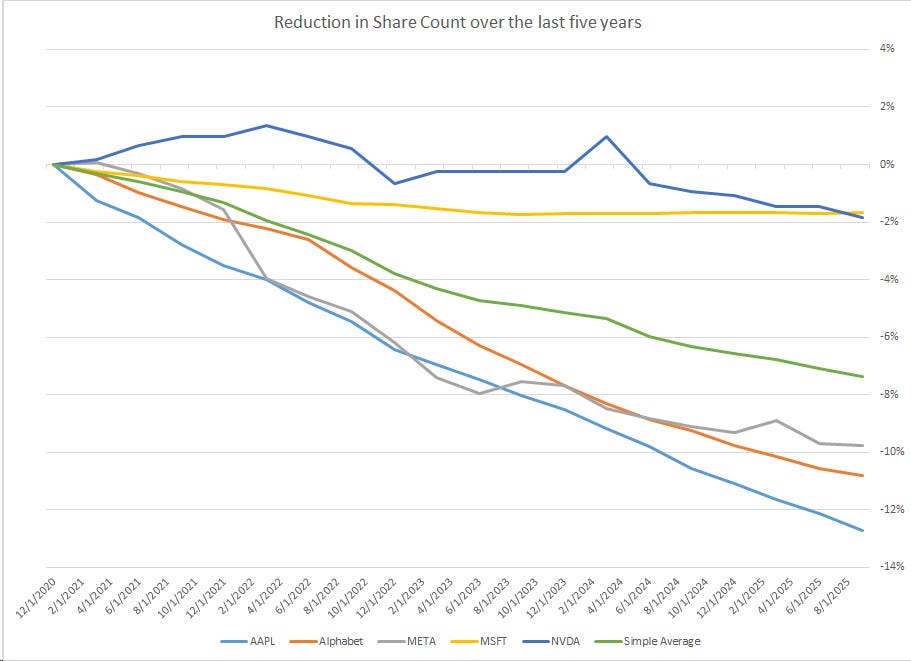

That dotted red line is one of the most dominant forces in the equity market. The light blue dotted line is slowly upward sloping which has offset the increased buyback activity ovetr the last twelve months but its clearly a losing battle. Of the biggest share repurchase programs all except Microsoft are decreasing share count actively.

The big question for 2026 is will share repurchase which net retire shares slow or stop altogether as promises for AI Capex need the cash that would otherwise have been spent on share repurchases. AAPL has limited plans or promises, NVDA has had no trouble reducing share count aggressively lately but the question of “circular” funding deals creates some risk. Meta and Alphabet share count reduction is slowigng.

So to be bullish equities based on supply and demand one only has to expect that savers will generate new demand above expectations and share repurchase supply contraction will continue at above expectations levels. Of all the reasons to be bullish stocks the supply and demand imbalance is the most compelling to me. Nonetheless pay attention to savings accumulation by households, leveraging up buy financial asset investors, companies using their cash flow for AI infrastructure instead of share buybacks, and changes in ipo’s and secondary issuance to gauge this bullish back drop.

The final driver of risk premiums is the availability and cost of credit to allow investors to make leveraged asset purchases. When you look at the last section you may think heck. I buy stock and sell to these passive flows and into corporate buybacks. Free money. Unfortunately this is where expectations play into investing. A great example is if a pension fund expects inflows from their savers they can buy ahead of that flow. If a hedge fund expects corporate buybacks to reduce supply they can frontrun the buying. All it takes is financial leverage. If investors and leverage providers are underleveraged they have capacity to front run these flows. If so the current price already reflects the future flows. If however investors are overleveraged and those flows dont come in as planned the deleveraging of investors can cause a bearish move despite very clear bullish supply and demand. If investors leverage up that is bullish equities

Where are we today?

To be bullish stocks based on risk premium contraction one has to expect

Risk to fall relative to current expectations

Savings to grow faster than expectations driven by nominal growth above expectations

Issuance net of buybacks to be more negative than expectations

Investors leveraging up.

Lastly the public sector budget deficit, tax policy and debt management has to net result in less long term treasuries than expectations

C’mon anchors matter don’t they?

I gave you many many bullish cases for equities today. Of course it should be noted that literally every one of those bullish cases can be flipped to a bearish case. Thats why the anchoring game to a particular outcome is so useless. No one knows whats going to happen. If you really want to try to time markets, which I strongly suggest you reconsider your time usage, it actually does pay to have an anchor or two or ten. In order to take money from someone else that is more than just luck you absolutely have to have a view that markets are mis-priced. I suggest you don’t use a hard target but instead think of all the various pressures and drivers and assign a weight and sign to each. Is growth bullish or bearish, is inflation bullish or bearish, are risk premiums likely to contract or expand? Add up the pressures on equities and take a position if thats your gig. Then without a target in mind continue to do this every day until the pressures change. BUT these anchors you place can not be deep and overweight. Remain humble and assume the market is right.

Dammit Andy are you bullish or bearish?

I think 2026 will be a very unusual year. At this moment my views are not particularly strong.

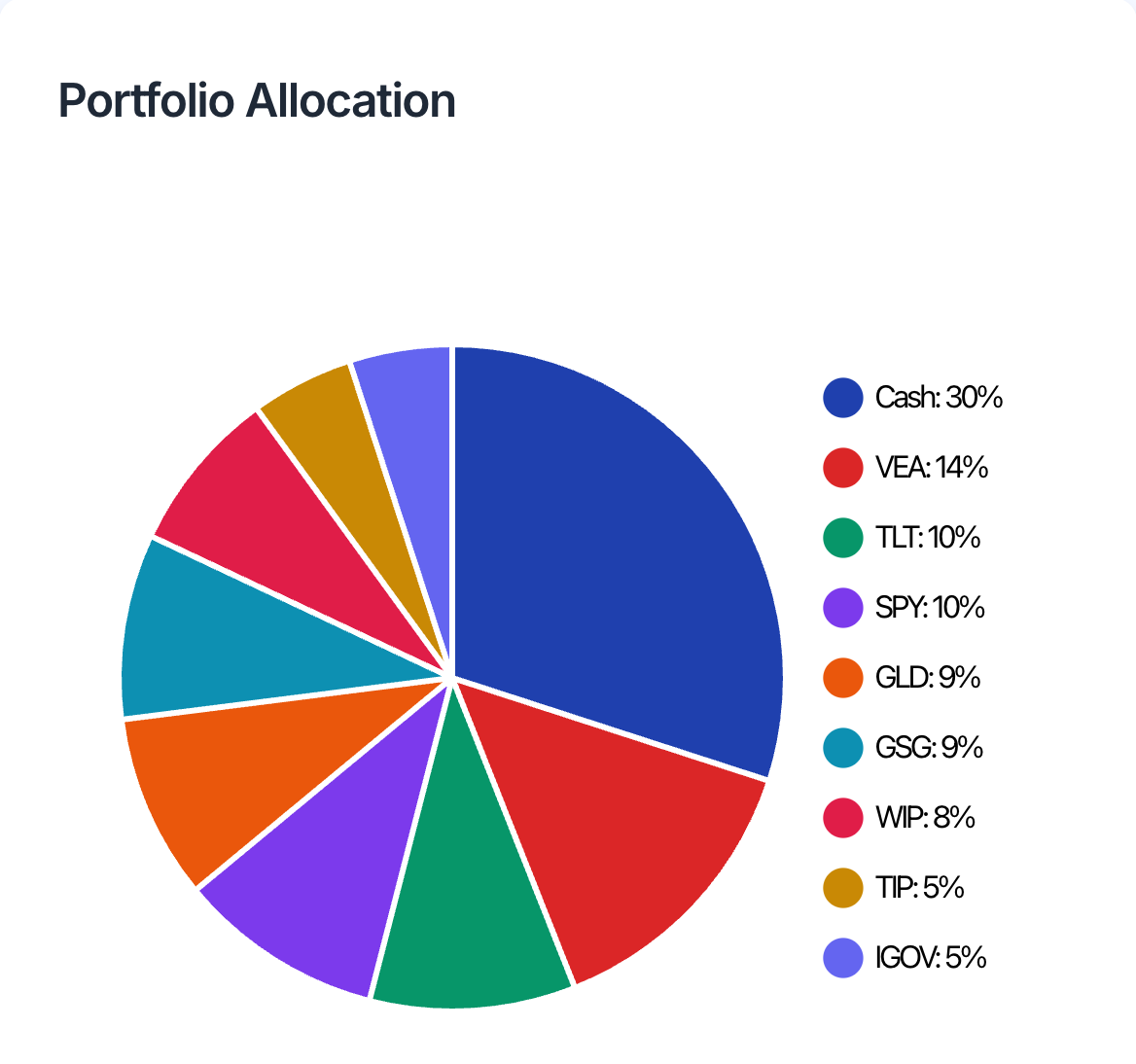

I am overweight cash in my long only beta portfolio but also overweight gold , commodities, and non US equities. I am severely underweight US bonds and somewhat underweight US Equities

.

For my alpha portfolio I have a very strong view on short term US interest rates as I expect the Fed will cut more than is currently priced into markets. I also have a 1/4 Max position (Tiny) short SPX and short Ten Year bond position

Net net I am conservatively positioned and will likely remain so until the SCOTUS ruling and the naming of the new Fed Chairman. BUT I expect to remain very long STIR and build a very large short US Equities and US Bonds in my Alpha account as these events unfold.

If you want to see me put the above framework in action join DS Read at dampedspring.com. There I go into detail about all I’ve described above and what my outlook is on each driver. It adds up negative today but that is just as irrelevant as any other year end forecast.

Andy - Thank you! I agree that longer term bond yields may increase (short 10yr), what are your thoughts on 30 Yr TIPS? They are near 15 year highs for real yields and I’ve been adding (~5% of portfolio).

Would love your thoughts on my post regarding TIPS:

https://open.substack.com/pub/eric5280/p/dont-be-foolish-protect-your-wealth?r=217g9x&utm_medium=ios

Andy, thank you for this! I appreciate you taking the time to share your thoughts. I know I will revisit this a dozen times!

I'm already re-visiting this sentence - "Of all the reasons to be bullish stocks the supply and demand imbalance is the most compelling to me."

This sticks with me because of a recent substack article by Michael Burry in which he references, (and I'm sure I'm oversimplifying his point), how megacap buybacks have barely kept pace with stock based compensation (SBC) and have actually eroded investor ROE over the long term because of net dilution by SBC. So, if (and I know it's a big "if"), the supply of buybacks continues to fall, and SBC does not fall in tandem, investors will be further "diluted" by SBC and investor ROE suffers even more. My gut says that's bearish.

Am I close here? Or, am I conflating to unrelated things?

Again, thank you for this article!