Risk Premium 201

Levels of risk premiums are useless. Drivers of risk premium changes are useful.

Readers of the dampedspring twitter feed and DampedSpringReport (DSR) may have noticed that we spend a great deal of time talking about risk premiums. Over the last 5 years we believe that understanding risk premiums and more importantly the drivers of risk premium have been critical for navigating the financial markets. Despite providing educational work on the topic for years we continue to see confusion in financial markets regarding the topic. This article will hopefully clarify why we care about risk premiums and how we use them for allocating to both our DS Smart Beta and DS Alpha portfolios.

Perhaps the most important confusion we want to clear up is that the level of risk premiums (called term premium in bond markets) has almost no predictive value for short, medium or even long term asset returns. The level doesn’t much matter at all for trading markets. What matters a great deal is drivers for changes in risk premium.

Said another way the level of risk premiums at any one moment are simply an outcome of market pricing like any other valuation metric. Similar to P/E for equities, curve steepness for treasuries, credit spreads, implied volatility for options, growth expectations, or inflation expectations, risk premiums are coincident to price. All of these things are essentially valuation metrics. Some believe that valuation is an important aspect of investing, we agree that it is a factor for an investor however valuation is a lousy signal for future returns on most all horizons. Valuations can stay “Rich” for many years. Same goes for risk premiums.

Let’s briefly review risk premium definitions and the root cause why risk premiums are likely to exist.

Damped Spring Twitter Risk Premium 101

One of the big complaints by those who criticize the use of risk premiums is that risk premiums are unknowable. We agree that risk premiums are unknowable. However, we would add that all investment drivers are unknowable. Let us expand. First here is a brief thread on our investment framework for asset class drivers.

Damped Spring Twitter DS Investment Framework 101

Our Framework posits that all asset classes are driven by common factors

Changes in Growth Expectations

Changes in Inflation Expectations

Changes in Risk Premiums

Flow and positioning

Idiosyncratic risk within an asset class or across countries

We don’t know what the level of risk premium is today. It is unknowable and one must revert to models to estimate risk premiums. But, the same can be said for both growth and inflation expectations. These two factors are estimated and modeled and market prices of assets are sometimes used to tease out expectations but those models and estimates are no better than used for risk premium levels.

So what we do is recognize that the levels of risk premium, growth expectations, and inflation expectations are unknowable AND more importantly if known they are not useful to begin with as they are coincident valuation metrics. None of these factors are predictive of future returns. Nonetheless if one can understand what drives changes in these factor the levels are mostly irrelevant. If one can understand the driver of change one can then understand the driver of asset prices and perhaps have a lead on price changes of investable assets that provides alpha.

Why is this our framework for investing. We see three major questions an investor needs to consider.

Should they prefer long term assets or cash (Money Market Funds or Tbills)?

Should they prefer stocks to bonds when allocating to assets?

Should they prefer nominal or real future cash flows when allocating to assets?

Question 1 is answered by determining the direction (not the level) of risk premiums.

Question 2 is answered by determining the direction (not the level) of growth

Question 3 is answered by determining the direction (not the level) of inflation

Down a level positioning and flow and idiosyncratic risk within an asset class and across countries also plays a part in smaller questions of timing and diversification but these 3 questions dominate asset allocation decisions in our humble opinion.

All of the levels that one needs to know are unknowable and irrelevant for making active investment allocations.

So what?

We are strong believers that almost all investors shouldn’t even try to make active investment allocations. Furthermore we believe that a portfolio of assets can be built that can diversify away most of the risk of inflation and growth changes. A portfolio with a balance of pro and anti growth assets and pro and anti inflation assets is our desired passive beta portfolio. Unfortunately the one thing that cannot be eliminated is the exposure to changes in risk premium. Every long term asset benefits from falling risk premiums and suffers from rising risk premiums. The only form of savings that has no exposure to risk premium is cash or cash substitutes. Nonetheless it is very very unusual for risk premiums to be so low (or even negative) such that we would advocate cash over a diversified balanced to growth and inflation asset portfolio. Answering the first question on should an investor prefer long term assets to cash is almost always YES. For most investors that answer should remain yes for their investment life.

With extremely important preamble we will now turn to active management of a portfolio. The basic decisions to make in an active portfolio are

Hold more or less assets vs holding cash.

Hold more growth assets or more anti growth assets

Hold more nominal cash flows or real cash flows.

In order to make these choices one needs to predict changes in risk premiums, growth expectations, and inflation expectations respectively. Remember the level of each of those things is a “valuation metric” and the determination of that level is impossible. We don’t even try. We certainly have models for every one of these factors, in fact we have multiple models for each factor. But we don’t much care about the level.

This article is about risk premiums and for that reason we will narrow the topic to factors that drive risk premium and save factors that drive the other two unknowable expectations levels and their impact onasset return for another day.

Talking past each other

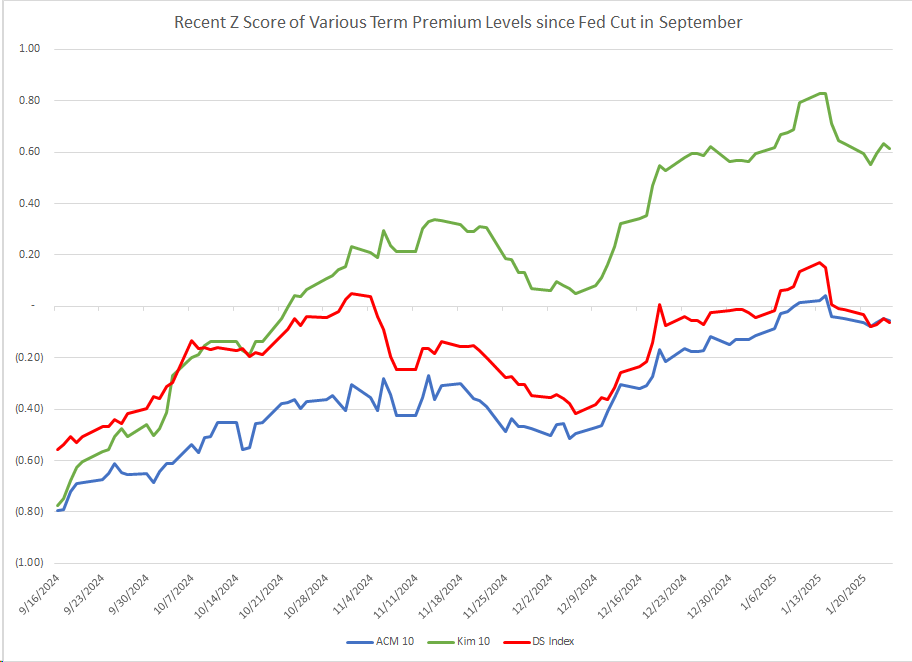

We interact on Twitter with many great thinkers. Risk premiums have become a hot topic in markets as various classic models have shown an increase in term premium levels in the US Treasury markets.

Our own model which uses a lowish weigh in these two classic models and many other market based and non market based metrics has also risen. But again these models are coincident and not predictive.

A number of smart people suggest that these models are 90% replicated by the slope of the 2’s 10’s curve or other formulations. WE AGREE. We also believe that the 2’s 10’s curve is coincident and not predicitive.

Other smart people suggest that the level of risk premium is driven by the diversification benefits of portfolio assets. In other words risk premiums have risen because portfolio diversification benefiit has fallen. WE AGREE. We also believe that in order to understand change in asset prices means one cannot look backward at asset covariance and instead must predict forward portfolio risk. Our framework for changes in risk premium rests heavily on future asset volatility and asset correlations.

The last voice we greatly respect suggests that the US Treasury curve has a negative risk premium. He believes the risk free rate is better ascribed to a different pool of assets specifically government guaranteed mortgage bonds. We can absolutely appreciate that idea while not fully agreeing. The implication is the treasury curve offers a lower than expected return vs the risk free curve and by definiton must carry a negative risk premium.

We ourselves believe strongly that various asset classes have low or even negative risk premiums. Assets like gold offer investors a unique diversification benefit and for that reason a negative expected return vs cash is tolerable. It is also likely if not certain that various savers have structural demand for certain assets that far exceeds the supply of that asset resulting in persistent negative risk premiums.

All these smart people are talking past us. They are explaining the level of risk premiums. Either they are using a different model for that level, a backward looking driver of the level, or are suggesting that the levels are simply massively wrong. WE AGREE with all of these people. BUT that is not what we care about at all.

Making money in active asset allocation is dependent on the change in risk premiums not the level. We don’t care about explaining the level, modeling the level, or even the level itself. What we care about is whether the level is likely to rise or fall.

Our framework

As mentioned in our 101 above we believe that risk premiums are paid to savers from borrowers such that the saver will give the borrower cash and get an asset back in return. The very next moment the saver is exposed to a change in the price of the asset and thus has risk. If for any reason they need cash they will only be able to raise cash by selling the asset. Is the level of excess return vs cash adequate to make that deal. Almost all the time it is. Can the saver allocate to many different assets and collect the excess return from each while taking less risk via diversification benefits? Yes they can. Nonetheless the deal offered depends on some key drivers.

The available money and credit from savers vs the supply of assets from borrowers

The expected risk of each asset

The expected diversification benefit of holding multiple assets in a portfolio

When savers want risky assets and have cash or credit to buy them they tend to push up assets prices. In other words push down risk premiums. When the forward expectations of an assets risk falls that creates demand which pushes down risk premiums. When diversification benefit is high that creates demand for all assets which pushes down risk premiums.

Similarly when assets are more risky, more correlated and issuers in the primary market and owners in the secondary market want to sell savers expect a much better deal and risk premiums expand.

Factors worth considering for your own risk premium change analysis.

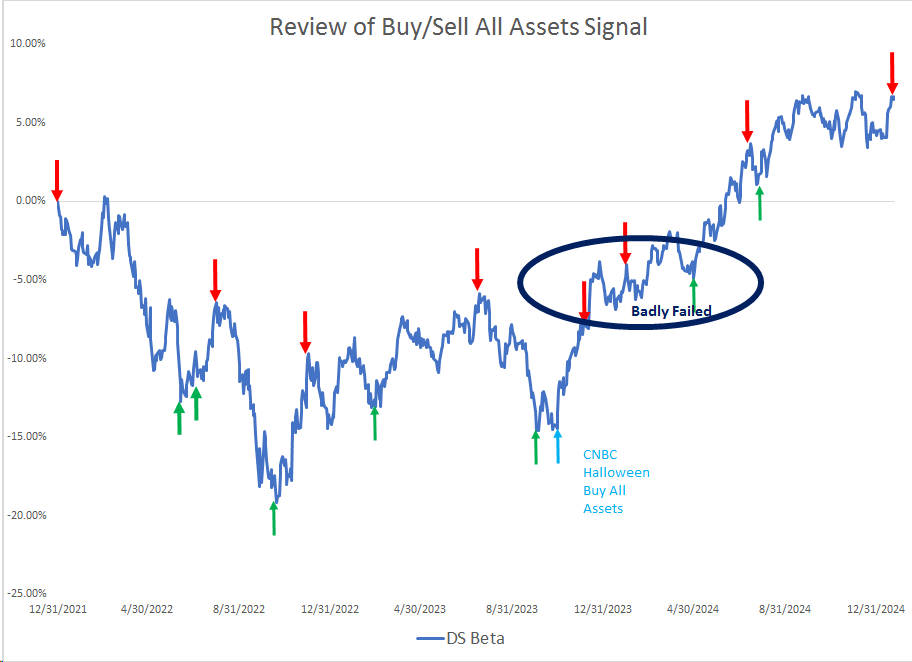

DampedSpring considers risk premium forecasting as our highest alpha signal and biggest differentiator. Our signal has been quite successful for us. Not perfect but pretty good.

Unfortunately we are unwilling to give our indicators away. However we are happy to share some key inputs into our work

Expected volatility of each Asset

Correlation expectations

Asset supply and demand across all cohorts

Central bank actions

Fiscal actions

Private sector leverage

Asset performance and investor “pain”

Health of leverage providers

Returns available to leverage providers

Economic factors that result in changes in savings accumulation

Taxes

Momentum and mean reversion of many if not all of these inputs

We think owning a balanced set of assets and collecting risk premiums passively is what almost everyone should be doing. We also take a highly data dependent approach to evaluate the drivers of changes in the “unknowable” levels of risk premium to help us allocate from/to assets vs cash for our active strategies. Not covered here we also consider the drivers of changes of the equally “unknowable” levels of growth expectations and inflation expectations in order to allocate across pro growth, anti growth, real, and nominal assets.

We don’t care much at all about the levels of risk premiums, growth expectations, or inflation expectations. We don’t bet that the market is fundamentally mis-valued today or any day. We do attempt to predict how levels change.

We hope this helps