The Ultimate Anchor

Ultra long interest rate dynamics and the 50 year mortgage

I thought I would write down some thoughts on long term interest rates as it has some relevance given the 50 year mortgage stuff running around. For that particular topic see here

However, long term interest rates in general are an interesting topic worth thinking about. The Damped Spring Framework assumes long term risk free real interest rates are anchored real growth and real growth’s principle drivers of employment growth (population) and productivity growth. Nominal interest rates are “less anchored” as inflation is a policy choice. But inflation targeting provides some level of “anchor”

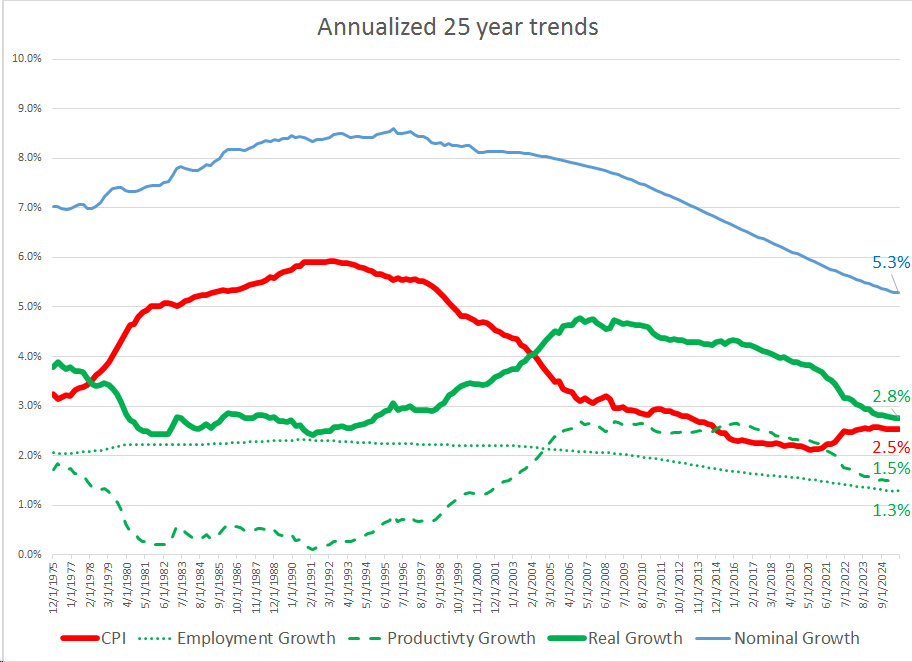

When looking at long term annualized real growth we can see real growth is trending lower driven by declining population growth which globally is a combination of long term fertility trends offset modestly by increases in worker retirement age. In the US employment growth has been buoyed as compared to the rest of the DM and China by immigration. Productivity boomed over the past two decades as the internet age fed into all of our work.

Nominal growth has largely tracked real growth except during the 70’s and 80’s.

So one possible anchor for long long term risk free real rates is to extrapolate the current levels of productivty and employment growth into the future which would augur for a 2.8% real 50 year rate. Inflation is sorta of a crapshoot but frankly even if the target is no longer 2% just extrapolating current long term average would suggest a nominal rate of 5.3%

Bigger point

Basically I think of the yield curve like a boat anchored at sea. The anchor is in soft sand that generally holds firm but is subject to some slippage as major major long term trends evolve. But that anchor is extremely far from the surface and is mostly conceptual. On the surface the short term shifts of the economy cause wild swings in yields. The Fed generally attempts to dampen those swings with monetary policy. Down at the 5 year depth the swings are quite noticeable. Even down to 30 year depth real yields and inflation expectations are not quite anchored to real long term growth trends nor are inflation expectations truly anchored. But somewhere deep beneath the surface an anchor exists that sticks pretty close to the long term trends. Is that 50 years? Hard to say. Certainly the 50 year depth is probably pretty close to the sand but 50 years still has some generational bias. The anchor likely is at a multigenerational depth.

The anchor does shift in the loose sand.

While the anchor holds firm enough to constrain the boat and the whole “yield curve” anchor line during most of the short term swings it is absolutely not fixed. Perhaps the biggest shift that has been occuring is fertility. Real employment growth is in a secular downtrend which has very little chance of reversing in the next century. My view on productivity is that can grow and has grown in the past. At the same time there are real world constraints on productivity historically which mean productivity bursts are real and persistent but need the next “invention” to sustain themselves. Over the past centuries productivity bursts have occured a few times. They create meaningful bursts which impact the ship on the surface and the down many years in depth. But its seems unlikely that the next 100 years of productivity growth will be much different than the past 200. The anchor could shift higher in yield if I am right but that may be offset by even slower employment growth.

Long term bond yields

So as mentioned the longer maturity a bond has the lower its sensitivity to surface chop and the higher its sensitivity to the anchor. A 30 year bond is NOT anchored. Furthermore a 30 year bond discounts where the anchor will slip to. It already discounts the employment growth secular down trend. a 50 year bond will be ever closer to the anchor but its hard to justify given current 5.3% Nominal 25 year growth that it will be lower in yield than the 30 year. at 4.7% today.

Supply and demand

One thing is certain about the 50 year bond. There is no supply. However much is made about the need for insurance companies to match Life policy long duration obligations. They have demand. Perhaps even more relevant the insurance company wants duration and a 50 year bond offers more duration for the same dollar investment. There is a very strong possibility that supply of 50 year bonds would result in a swap by insurance companies from 30’s to 50’s which would place downward pressure on 50’s yields BUT would come at the cost of upward pressure on 30’s yields. Gun to my head with an anchor at 5.3% which is likely slipping lower to 5% or lower the 50’s and 30’s would settle at 4.9% once large supply comes to market.

Anchors Aweigh :)

Unrelated I know. But do you think you could do a write up on the current state of "the script"

Also I enjoyed the anchor analogy